You will need

- - credit agreement;

- calculator;

- - Excel

Instruction

1

Take the loan agreement and find the paragraph on the rules of calculation of the interest on the loan. As a rule, the payment schedule is of two types: classic and annuity. Classic graph assumes interest payments in the amount of the monthly body of the loan and every month payment is reduced by a certain amount. Annuity schedule is payment of interest and each month the same amounts that do not change until the end of the loan period.

2

Find it in the contract the initial amount of the loan, term in months, if specified in years, turn, multiplied by 12 and the annual rate in percent. Check all associated one-time and monthly Commission according to the text of the Treaty. If the loan the Bank required collateral to insure — write the amount of payment for insurance.

3

Now, to calculate the repayment of classical type take a calculator, sheet of paper and then calculate by the formula: interest = (total loan amount) / (loan term in months) x (annual interest rate) / 365 x (30 or 31 [days, months]). You will get the payment on the interest for the first month. To calculate each subsequent payment should initial the amount of change in the balance of the loan. The monthly payment on the loan is even easier: monthly payment = (loan amount) / (loan term in months). Total monthly payment = (monthly payment body) + (interest).

4

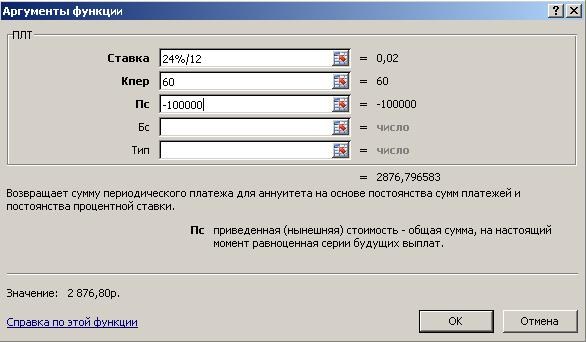

Schedule for an annuity is calculated is more complicated. It is better to use the program Excel to not tormented with the calculations manually. Open the Excel sheet and in any cell put = and then select the PMT function. For example, your loan is 100 000,00 R., at 24% per annum for 60 months, enter in the popup list of the following values:

5

Press "OK" and you will receive your monthly annuity payment. If you enter manually it would look like the following:

=PMT (24%/12; 60; -100000). In brackets enter the indicators of need in the following order: interest rate, number of months loan, the initial amount of the debt. A minus in front of 100 000 means the obligations of duty, if not to deliver the final value will simply be negative.

=PMT (24%/12; 60; -100000). In brackets enter the indicators of need in the following order: interest rate, number of months loan, the initial amount of the debt. A minus in front of 100 000 means the obligations of duty, if not to deliver the final value will simply be negative.

6

To understand the full amount of the overpayment on the loan it is possible to calculate so-called effective rate. Effective interest rate = ([loan + interest for the entire period + Commission] / loan term in years) / average loan amount. Average loan amount: loan amount x (loan term in months + 1) / (2 *term of loan in months). In the end, you find out how much really is the real interest rate on the loan.

Note

Note that any value set monthly fee on the loan (from initial amount or balance); is there any fee for early repayment of the loan;

Useful advice

Be sure to choose the Bank in which interest on the loan is happening in the rest of the body, and not on the initial amount.

Before election of annuity schedule check if there are any penalties for early repayment.

Before election of annuity schedule check if there are any penalties for early repayment.