You will need

- To receive a property deduction at the end of the year, must be submitted to the tax Inspectorate by place of residence:

- Filled the tax Declaration under the form 3 personal income tax.

- The application for refund of personal income tax in connection with the acquisition costs of property, with indication of requisites for transfer of the sums of return.

- A certificate from the accounting Department at the place of work of the amounts accrued and withheld taxes for the year on form 2-NDFL.

- Copies of the documents confirming the right to housing (certificate of state registration of rights, the agreement on the purchase of housing, the instrument of transfer of the apartment, credit agreement or loan agreement, mortgage agreement, etc.).

- Copies of payment documents confirming expenses on the acquisition of property (receipts to credit orders, Bank extracts about transfer of money resources from the account of the buyer to the seller, commodity and cashier's checks and other documents).

- Documents attesting to the payment of percent on the target credit agreement or the loan agreement, the mortgage agreement (extracts from personal accounts, certificates of the Bank about the paid percent on the loan).

- A copy of the marriage certificate (if housing is purchased in joint ownership).

- A statement on the distribution of property tax deduction (if housing is purchased in joint ownership).

Instruction

1

Download from the website the tax office and install the software for filling return for the required year.

2

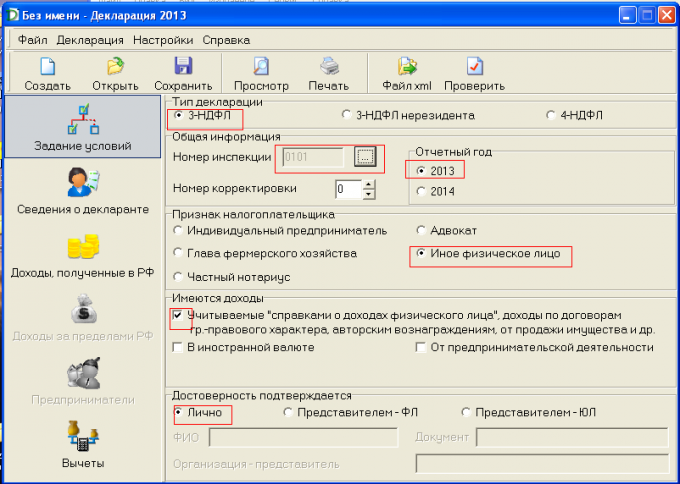

Open the program. The program opens the tab "setting conditions". Fill: the Declaration type of inspection (choose from the list), reporting year, a sign the taxpayer's available income proof of the reliability.

3

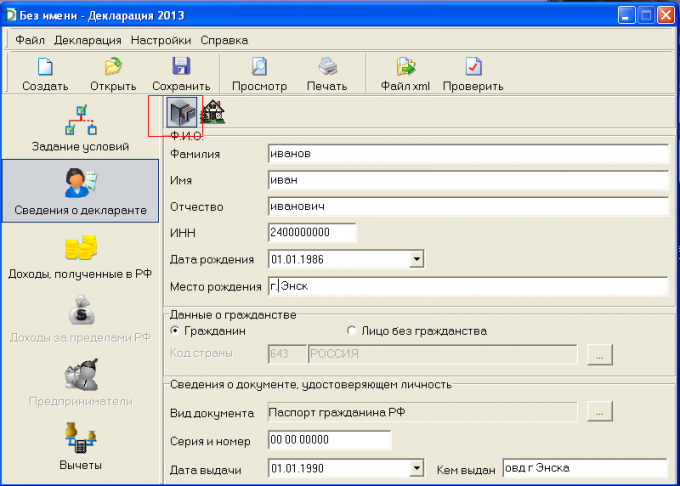

Go to the tab "details of the declarant". Fillable personal data.

4

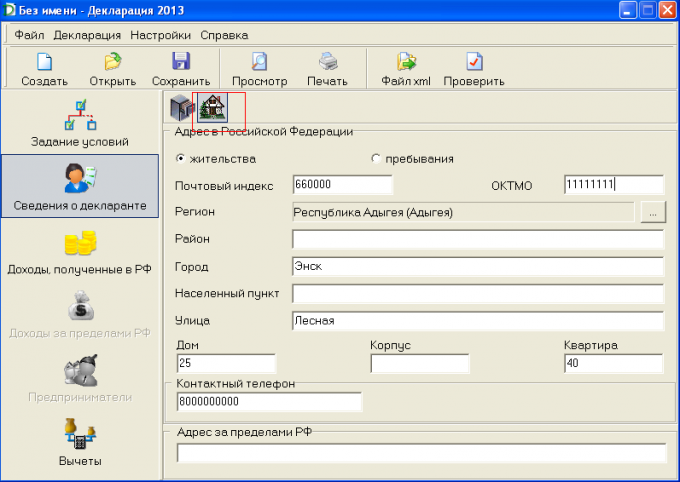

Click on the image "house". Turn to fill ' (as in passport). In 2013, the indicator "the Code on OKATO" is replaced by "Code OKTMO". On the website of the Federal tax service of Russia hosted email service "Know OCTO,". It allows you to determine the code of OCTO code OKATO, by name of the municipality, as well as using dictionary data ", Federal information address system (FIAS)".

5

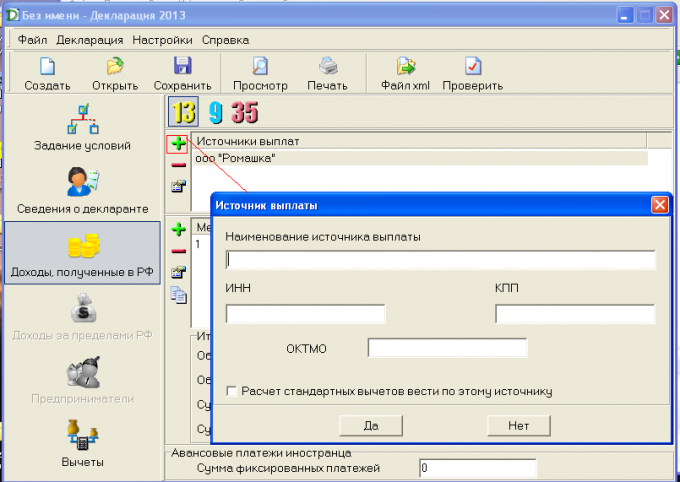

Go to the tab "Income received in Russia." Next to the window "source of payment" click on the "+" sign and fill in the employer information (information taken from reference 2 personal income tax).

6

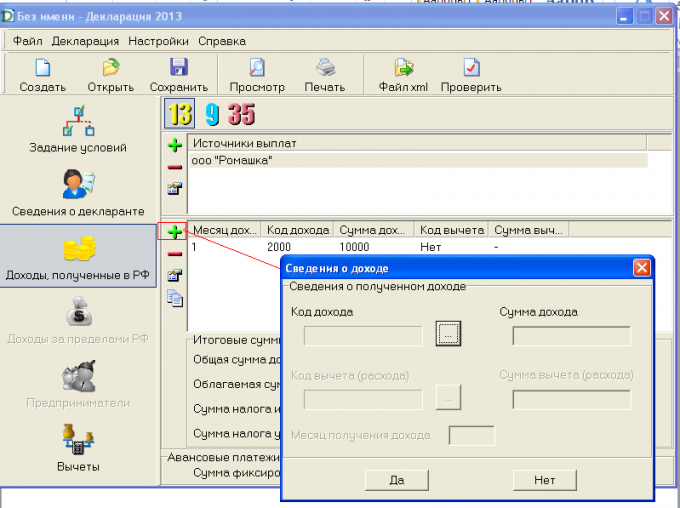

Similarly, fill in the table with income. Click on the "+" and fill in: income code amount of income deduction code, deduction amount, month income. Information taken from reference 2 NDFL.

7

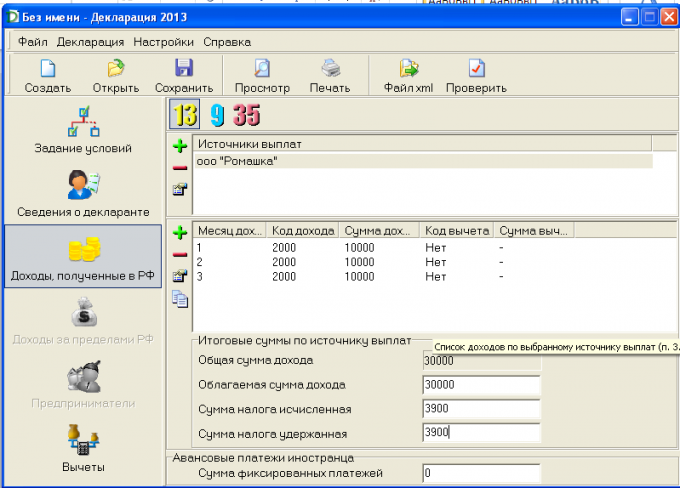

Fill in the column under the table income. The total income will be automatically calculated by the program. Taxable the amount of income tax amount calculated, the amount of tax withheld - fill yourself (information from reference 2 personal income tax).

8

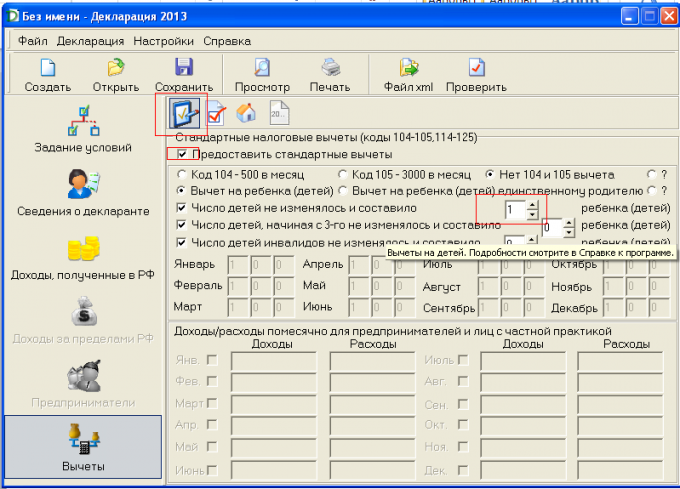

Go to the tab "Deductions". Put a tick in the box "to provide a standard tax deduction", you specify what deductions are available to us (information from reference 2 personal income tax).

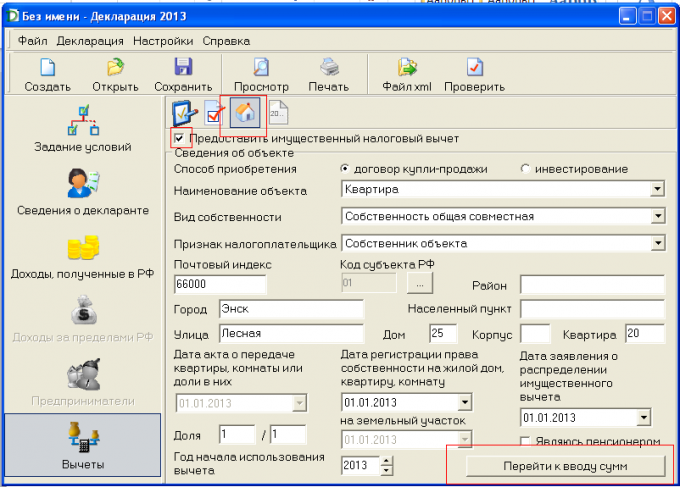

9

Click on the image "house". Populate the data on the acquired housing. Click on the "go to input amounts".

The filling of the form of ownership and share of the marital property.

Look at the certificate of ownership:

- property equity (the share is clearly identified); - the property deduction is provided to the fraction change its size;

- joint property. No matter who is recorded in the certificate as the owner if the apartment was acquired during the marriage, joint property is recognized in accordance with the Family code of the Russian Federation (article 33, 34 SK the Russian Federation). As a General rule, the deduction shall be divided in equal shares (50%), but spouses have the right to redistribute it in any proportion, giving the tax office a Statement about the distribution of the shares (in any form).

The filling of the form of ownership and share of the marital property.

Look at the certificate of ownership:

- property equity (the share is clearly identified); - the property deduction is provided to the fraction change its size;

- joint property. No matter who is recorded in the certificate as the owner if the apartment was acquired during the marriage, joint property is recognized in accordance with the Family code of the Russian Federation (article 33, 34 SK the Russian Federation). As a General rule, the deduction shall be divided in equal shares (50%), but spouses have the right to redistribute it in any proportion, giving the tax office a Statement about the distribution of the shares (in any form).

10

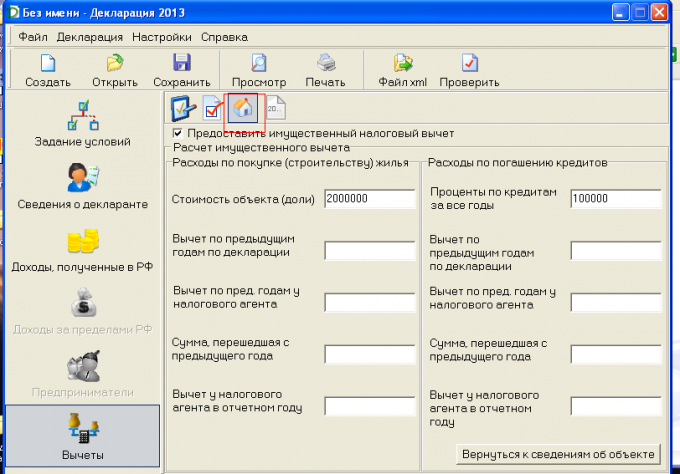

Fill the costs of buying a home and repayment of the loan.

The size of a property deduction.

For housing acquired before 1 January 2014, there is a limit of total deduction on the property in the amount of 2 000 000 rubles. This means that if you spent more than this amount, it will still get the deduction in the amount of 260 000 rubles (13% of 2 000 000 RUB.) and that this amount will be divided between the spouses in the case, if the housing is acquired during the marriage.

For housing, acquired after 1 January 2014, limiting the total deduction of 2 000 000 RUB applies to every citizen. That is, the husband may get a deduction with 2 000 000 (260 000 RUB.), and the wife may get a deduction with 2 000 000 (260 000 RUB.).

In addition to the deduction on the property, the citizen is based on the deduction on interest payment of loan taken for the acquisition (construction) of housing. The deduction for loan interest is distributed in the same proportions as the deduction. That is, if the spouses filed an application to the allocation of the deduction to 75% husband and 25% to the wife, the deduction for interest will also be provided in the amount of 75% husband and 25% to the wife.

For loans received prior to 2014, the amount of interest paid, which the government returns 13 percent income tax is not limited to, for loans received after 1 January 2014, the maximum amount of such costs 3 000 000 (i.e. you can return a maximum of 390 000 rubles.)

The size of a property deduction.

For housing acquired before 1 January 2014, there is a limit of total deduction on the property in the amount of 2 000 000 rubles. This means that if you spent more than this amount, it will still get the deduction in the amount of 260 000 rubles (13% of 2 000 000 RUB.) and that this amount will be divided between the spouses in the case, if the housing is acquired during the marriage.

For housing, acquired after 1 January 2014, limiting the total deduction of 2 000 000 RUB applies to every citizen. That is, the husband may get a deduction with 2 000 000 (260 000 RUB.), and the wife may get a deduction with 2 000 000 (260 000 RUB.).

In addition to the deduction on the property, the citizen is based on the deduction on interest payment of loan taken for the acquisition (construction) of housing. The deduction for loan interest is distributed in the same proportions as the deduction. That is, if the spouses filed an application to the allocation of the deduction to 75% husband and 25% to the wife, the deduction for interest will also be provided in the amount of 75% husband and 25% to the wife.

For loans received prior to 2014, the amount of interest paid, which the government returns 13 percent income tax is not limited to, for loans received after 1 January 2014, the maximum amount of such costs 3 000 000 (i.e. you can return a maximum of 390 000 rubles.)

11

If you previously filed the Declaration of 3 personal income tax, fill the corresponding columns. Deduction on the previous years returns - enter the sum of all previously filed returns (the amount you can be reimbursed for personal income tax, not the amount of the refund). The amount transferred from the previous year of the last filed return. Costs repayment of loans filled in the same way.

12

Click on the "view". Check, print, sign, and file tax with all necessary documents.

13

Property tax deduction (for the purchase of apartments and the payment of interest) can be granted before the end of the tax period. For this you need to contact the tax statement to receive the notice of right to a property deduction with the application copies of the documents confirming this right.

After 30 days of receiving the tax notice of the right to property as a deduction and give it to the employer. On the basis of this document, the employer will not withhold income tax, that is, the salary will not be taxed 13%.

After 30 days of receiving the tax notice of the right to property as a deduction and give it to the employer. On the basis of this document, the employer will not withhold income tax, that is, the salary will not be taxed 13%.

Note

1. Between spouses can be a marriage contract drawn up that specifies a special mode of ownership.

2. The deduction does not apply in the following cases: if the payment of housing produced at the expense of employers or other persons, of maternity (family) capital, and also at the expense of budget funds, and if the transaction of sale is concluded between interdependent persons (spouse, parents (including adoptive parents), children (including adopted), full and half brothers and sisters, guardian (Trustee) and ward.

2. The deduction does not apply in the following cases: if the payment of housing produced at the expense of employers or other persons, of maternity (family) capital, and also at the expense of budget funds, and if the transaction of sale is concluded between interdependent persons (spouse, parents (including adoptive parents), children (including adopted), full and half brothers and sisters, guardian (Trustee) and ward.

Useful advice

Keep copies of all filed your returns, it will make it easier to fill later.

Note 14.02.2015 in force the Order of the FTS of Russia, which approved a new tax return form 3-pit. Return for the 2014 tax take a new form to fill already appeared on the website of the tax.

Note 14.02.2015 in force the Order of the FTS of Russia, which approved a new tax return form 3-pit. Return for the 2014 tax take a new form to fill already appeared on the website of the tax.